Brexit and capital gain tax

Monday, 30 November 2020

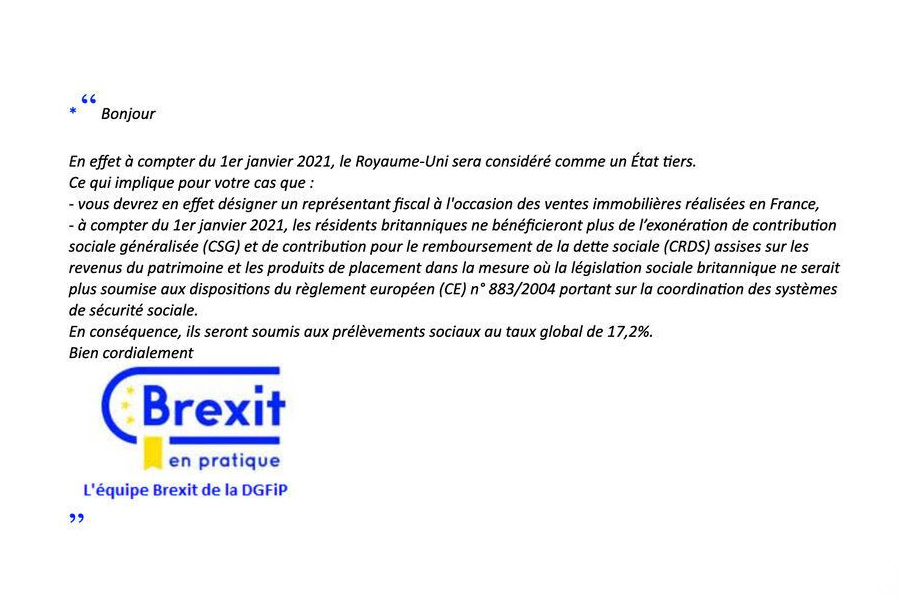

The French tax authorities have confirmed that from the 1st January 2021, the UK will be considered as a third state in the EU.

The French tax authorities have confirmed that from the 1st January 2021, the UK will be considered as a third state in the EU.

As a result, UK residents will no longer benefit from the treatment applicable to EU residents on two important aspects:

- they will have to appoint an accredited tax representative in France when they sell their French property (except for specific cases exemption);

- they will no longer benefit from the exemption of social levies (CSG and CRDS) and, therefore, the tax rate of 17.2% will apply to capital gains tax on the sale of a property completed from the 1st January 2021, making a total tax rate of 36.20%.

The French tax authorities have confirmed that from the 1st January 2021, the UK will be considered as a third state in the EU.

The French tax authorities have confirmed that from the 1st January 2021, the UK will be considered as a third state in the EU.

As a result, UK residents will no longer benefit from the treatment applicable to EU residents on two important aspects:

- they will have to appoint an accredited tax representative in France when they sell their French property (except for specific cases exemption);

- they will no longer benefit from the exemption of social levies (CSG and CRDS) and, therefore, the tax rate of 17.2% will apply to capital gains tax on the sale of a property completed from the 1st January 2021, making a total tax rate of 36.20%.